Corporate Transparency Updates for CBCA Corporations: New Reporting and Public Access Rules Effective January 22, 2024

The federal government has set January 22, 2024, as the effective date for new rules that will require non-exempt private corporations existing under the Canada Business Corporations Act (CBCA) to regularly report to Corporations Canada information regarding individuals who have significant control over their corporations (ISCs).1 Such non-exempt CBCA corporations that file their 2024 annual returns on or after January 22, 2024, will be required to report information contained in their registers of ISCs (RISCs). Similar filing obligations will be triggered upon incorporation, amalgamation and continuance as well as upon any change to information already reported. Also, significantly, Corporations Canada will be required to make publicly available some of the RISC information reported to it.

In this bulletin, we discuss the new filing and public access requirements, as well as related ancillary amendments to the CBCA, including increased fines for non-compliance.

As considered in a previous bulletin, these amendments form part of the federal government’s larger initiative to improve corporate transparency by creating a national, public and searchable beneficial ownership registry to combat money laundering, tax evasion and other financial crimes.

Who Will Need to File

The new requirement to report RISC information to Corporations Canada will apply to all CBCA corporations that are required to create and maintain a RISC. The obligation to create and maintain a RISC, which has been in effect since June 2019, will continue to apply separately from and in addition to the new reporting requirement.

CBCA corporations that are exempt from the requirement to create and maintain a RISC will need to confirm their exemptions with Corporations Canada. Exempt corporations include public companies existing under the CBCA (i.e., any CBCA corporation that is a reporting issuer under provincial securities laws or that has securities listed and posted for trading on a “designated stock exchange,” as defined in the Income Tax Act, which includes the Toronto Stock Exchange, the TSX Venture Exchange and senior U.S. exchanges), private CBCA subsidiaries that are wholly owned by a public entity (within the meaning of the CBCA) and Crown corporations.

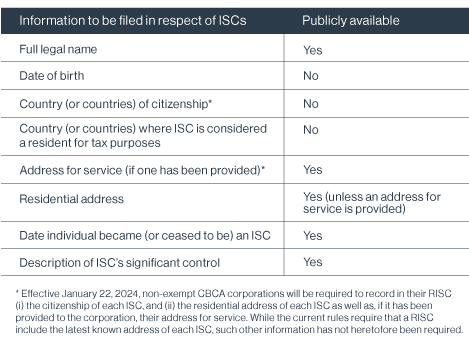

What to File and What Will Be Made Public

The CBCA amendments empower Corporations Canada to determine the RISC information that must be filed. These determinations have been set in recently published Guidelines, which provide that non-exempt CBCA corporations must file the following information in respect of their ISCs:

Effective January 22, 2024, Corporations Canada will be required to make available to the public the RISC information listed as publicly available in the table above. The rules also permit further RISC information to be made publicly available by way of the regulations. An exemption from publication will be available for information relating to an ISC who is under 18 years of age or to whom yet-unpublished prescribed circumstances apply. An exemption may also be sought on application in certain circumstances, including where publication presents a serious threat to the safety of the individual or in cases of incapability.

To link the collection of beneficial ownership information to the underlying enforcement objectives of the transparency rules, the amendments also authorize Corporations Canada to disclose all or part of the RISC information to the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC), investigative bodies, such as the police and Canada Revenue Agency, or such other prescribed entities. As well, Corporations Canada may provide RISC information to the provincial agencies or departments responsible for corporate law and compliance in their jurisdiction.

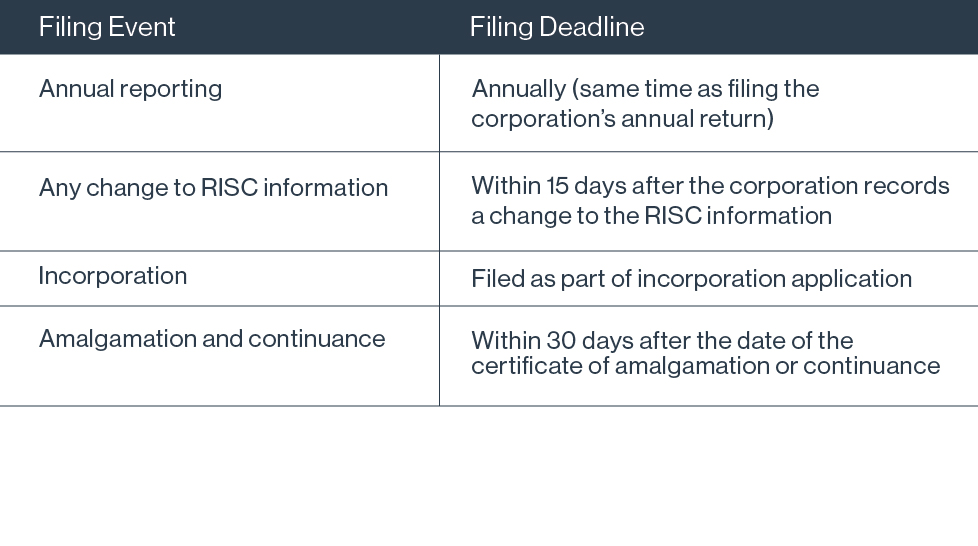

When and Where to File

Starting on January 22, 2024, non-exempt CBCA corporations will be required to file their RISC information through Corporation Canada’s Online Filing Centre at the following times:

We understand that the corporation’s access key to the Online Filing Centre will be required to submit ISC filings. Corporations that have misplaced their access key may contact Innovation, Science and Economic Development Canada for assistance.

Other Changes to the CBCA’s Corporate Transparency Rules

Other important amendments to the CBCA’s RISC rules will come into force on January 22, 2024.

- Penalties and offences. A corporation that contravenes the new reporting requirements “without reasonable cause” is guilty of an offence and is liable on summary conviction to a fine not exceeding $100,000. The penalty for directors, officers and shareholders who knowingly contravene the CBCA’s requirements to keep accurate RISC information and disclose it as required (including, for directors and officers, knowingly authorizing, permitting or acquiescing in respect of the non-compliance) has been increased from a fine of up to $200,0000 and/or imprisonment up to six months to a fine of up to $1 million and/or imprisonment up to five years.

- Dissolution and status certificates. Corporations Canada may dissolve a non-compliant corporation in certain circumstances and may refuse to issue a certificate of existence for any corporation in breach of the requirements.

- Increased authority for inquiries. Corporations Canada is currently permitted to make inquiries of any person relating to compliance with the CBCA and, effective January 22, 2024, will be authorized to require any such person to provide any records or other documents or information and to verify any information reported to it.

- Repeal of existing access rights for shareholders and creditors. The CBCA currently provides shareholders and creditors with a right of access to review and obtain an extract of a corporation’s RISC (see subsections 21.3(2)–(6)). These provisions will be repealed effective January 22, presumably in light of the new public access rules.

- Upcoming regulations on influence and control in fact? The new rules will permit regulations to be made prescribing what constitutes: (i) “direct influence,” “indirect influence” and “control in fact” for purposes of section 2.1(1)(b) of the CBCA, which provides that an ISC includes “an individual who has any direct or indirect influence that, if exercised, would result in control in fact of the corporation”; and (ii) “direct influence” or “indirect influence” for purposes of section 21.31(3)(c) of the CBCA, which provides investigative bodies with certain rights of inquiry, including with respect to ISCs who directly or indirectly influence the affairs of an entity. We note that Corporations Canada has published guidance on the meaning of “control in fact.”

- Whistleblower protection. The amendments will include a provision exempting Corporations Canada from having to disclose (other than to specified authorities) any information relating to the identify of a person who, “on their own initiative,” provides information relating to the commission of a wrongdoing under the CBCA, including a contravention of any provision of the Act.

- Updating RISC information. The current rules require that a non-exempt CBCA corporation must, at least once during each financial year of the corporation, take reasonable steps to ensure that the corporation has identified all ISCs of the corporation and that the information in the RISC is accurate, complete and up to date. Effective January 22, in addition to the annual requirement, Corporations Canada may at any time request a non-exempt corporation to undertake these steps.

What the Coming Changes Mean for CBCA Corporations

Non-exempt CBCA corporations that file their 2024 annual returns on or after January 22, 2024 will be required to report information contained in their RISCs. CBCA corporations that will be subject to the new filing requirement should ensure that their RISC is up to date to meet this deadline. Meaningful penalties will apply to contraventions of the new rules.

With the new requirement to make certain RISC information publicly available, the federal government will also need to make available the online interface through which access to the RISC information will be provided. Whether the provinces and territories, many of which have implemented or are implementing their own transparency requirements, will participate in the federal system to create a national interface remains to be seen.