In recent years, awareness of the potential impacts of climate change on issuers has heightened both in Canada and internationally. As the risks of, and potential opportunities associated with, climate change become better understood, investors and other stakeholders continue to press for greater transparency in climate-related reporting, expressing concerns about insufficient disclosure regarding these risks. In response to these developments, as well as the results of its 2018 CSA Staff Notice 51-354 Report on Climate change-related Disclosure Project (SN 51-354), on August 1, 2019, the Canadian Securities Administrators (CSA) published CSA Staff Notice 51-358 Reporting of Climate Change-related Risks (2019 Notice). The 2019 Notice provides guidance for reporting issuers to develop more effective disclosure of the material risks, opportunities, financial impacts and governance processes relating to climate change. The 2019 Notice does not create any new legal requirements; rather, it reinforces and expands upon the guidance previously provided in the 2010 CSA Staff Notice 51-333 Environmental Reporting Guidance (2010 Notice).

Current Regulatory Framework: Disclose Material Climate-related Risks

The continuous disclosure regime set out in National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102) requires reporting issuers in Canada to disclose material risks affecting their businesses and, where practicable, the financial impacts of such risks in their annual information form (AIF) and management’s discussion and analysis (MD&A). For purposes of these filings, information is likely material if a reasonable investor’s decision whether to buy, sell or hold securities in an issuer would likely be influenced or changed if the information in question was omitted or misstated.

The 2010 Notice, which continues to provide guidance to issuers on existing continuous disclosure requirements relating to a broad range of environmental matters, builds upon the rules for mandatory disclosure in NI 51-102 and how they relate to various environmental issues, including climate change. Under the 2010 Notice, five key disclosure requirements are identified: (1) environmental risks; (2) trends and uncertainties; (3) environmental liabilities; (4) asset retirement obligations; and (5) financial and operational effects of environmental protection requirements. With regard to governance, the 2010 Notice recommends disclosure of the board’s responsibility for oversight and management of environmental risks and any delegation of these responsibilities. The 2010 Notice sets out the following non-exhaustive guiding principles for making materiality assessments in respect of climate-related risks:

- No bright-line test. There is no uniform quantitative threshold at which a particular type of information becomes material; the materiality of information may vary between issuers and industries according to their particular circumstances. Issuers should consider both quantitative and qualitative factors in determining materiality.

- Context. Materiality depends on the nature and amount of the item, judged in the particular circumstances of its omission or misstatement. Materiality must be considered in light of all the available facts, not on a piecemeal basis.

- Timing. Assessing materiality is a dynamic process; an issuer should consider whether the impact of an environmental matter might reasonably be expected to grow over time, in which case early disclosure may be important to reasonable investors. This would be particularly relevant if the issuer is in an industry with a longer operation or investment cycle or if new technologies will be required.

- Trends, demands, commitments, events and uncertainties. As with other types of disclosure, materiality in cases of a known environmental trend, demand, commitment, event or uncertainty turns on an analysis of the probability of its occurrence and the anticipated magnitude of its effect.

The 2019 Notice reiterates these guidelines and should be read in conjunction with the 2010 Notice.

Increase in Voluntary Reporting and Use of Disclosure Frameworks

As stakeholder expectations on climate disclosure have heightened, a number of organizations have developed voluntary frameworks for the disclosure of climate-related risks. Leading disclosure frameworks include the industry-specific disclosure standards developed by the Sustainability Accounting Standards Board (SASB) and the recommendations of the Financial Stability Board’s Task Force on Climate-related Financial Disclosures (TCFD). The TCFD’s recommendations encourage disclosure of material information within four key categories: governance, strategy, risk management, and metrics and targets.

Although the voluntary disclosure standards prescribed by these frameworks often overlap with many of the requirements under securities laws, they contemplate more extensive disclosure than would be required under the securities law materiality standard. For example, the TCFD advocates the use of scenario analysis to assess the resilience of an issuer’s business strategy under different climate-related scenarios. It also recommends more specific disclosure relating to the governance and risk oversight of climate-related risks.1 The SASB framework encourages the disclosure of climate-related impacts that are reasonably likely to affect the financial performance or operating condition of a company.2 This standard is similar, though not identical, to that imposed on reporting issuers under Canadian securities laws.

The CSA has taken notice of the growing number of issuers voluntarily disclosing climate-related risks on their websites, in sustainability reports and in publications beyond those required under the continuous disclosure regime.While encouraging issuers to draw upon available voluntary disclosure frameworks, the 2019 Notice provides further guidance on the appropriate use of voluntary disclosure by issuers (as discussed further below).

2019 Notice: Climate-related Risks, Opportunities and Disclosure

As discussed in our April 2018 article, the CSA’s 2018 review of the mandatory and voluntary climate-related disclosure of 78 issuers from the S&P/TSX Composite Index revealed that just under half of these issuers provided boilerplate disclosure or no disclosure at all. The CSA also found a broad consensus among investors and other stakeholders that climate disclosure was largely deficient or incomplete. The ongoing release of generic, boilerplate disclosure by many reporting issuers led the CSA to issue the 2019 Notice to elaborate on its previous guidance regarding climate-related disclosure.

As noted above, the 2019 Notice does not create any new legal requirements or modify existing legal requirements and is intended to guide issuers in identifying material climate-related risks and improving their disclosure of those risks. The 2019 Notice focuses primarily on issuers’ disclosure obligations as they relate to the MD&A and AIF; it also acknowledges that while disclosure of material climate-related risks is important, it presents challenges and potential burdens for issuers, especially smaller issuers. Below are some of the key takeaways from the 2019 Notice. A complete copy of the 2019 Notice can be accessed here.

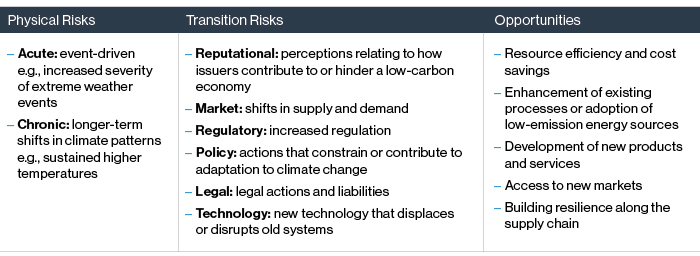

Categories of climate-related risks and opportunities. The 2019 Notice provides useful guidance concerning the categories of climate-related risks and potential opportunities that issuers should consider over the short, medium and long terms when disclosing climate-related information.

In addition, the 2019 Notice contains examples of risks that fit within the above categories and the potential operational and financial impacts that could be relevant for disclosure. It also provides questions for boards and management to consider in assessing the materiality of these risks. The 2010 Notice also includes examples of entity-specific disclosure that issuers may find helpful.

Conduct materiality assessments. Given that climate-related risks and their potential impacts are mainstream business issues, boards and management should take appropriate steps to understand and assess the materiality of climate-related risks to their businesses. This analysis should extend to a broad spectrum of potential climate-related risks, including physical risks and risks associated with the transition to a low-carbon economy, over the short, medium and long terms, as listed above. Management should assess, among other things, the current and future financial impacts of material climate-related risks on the issuer’s assets, liabilities, revenues, expenses and cash flows over each of these time horizons. Issuers are also encouraged to draw upon voluntary disclosure frameworks to assist them in making their materiality assessments. The 2019 Notice reinforces the guiding principles for materiality assessments in the 2010 Notice and adds the following guidance:

- Timing. An issuer should not limit its materiality assessment to near-term risks. If an issuer concludes that a climate-related matter would likely influence or change a reasonable investor’s decision whether or not to buy, sell or hold securities of the issuer, the CSA expects it to be disclosed. Disclosure should be made even if the matter may only crystalize over the medium or long term or if there is uncertainty whether it will actually occur. Even if the likelihood of the risk occurring diminishes the materiality of the matter, issuers should still consider whether to disclose the matter as a risk factor.

- Measurement. As part of a materiality assessment, issuers should, where practicable, quantify and disclose the potential financial and other impacts of material climate-related risks. In certain instances, existing securities laws may require the quantification of these types of risks. In other cases, issuers should consider how to effectively measure and quantify climate-related risks as part of their broader risk assessment process. The CSA is of the view that issuers should consider both quantitative and qualitative factors in making their materiality assessments and may consider using assumptions and estimates that have a reasonable basis and are within a reasonable range. External resources and benchmarking against industry peers may also be appropriate.

Establish expertise of boards and management. Boards and management should assess their relative expertise with respect to sector-specific climate-related risks to enable them to make informed decisions about risk management and disclosure.

Provide meaningful entity-specific disclosure. Boards and management should avoid vague or boilerplate disclosure. Disclosure should be relevant, clear, understandable and entity-specific so as to assist investors in understanding how the issuer’s business is specifically affected by all material risks resulting from climate change. Risk disclosure should also provide context for investors about how the board and management assess climate-related risks.

Create board oversight of climate-related issues. Boards should consider whether the methodology used by management to capture the nature of climate-related risks and assess their materiality is appropriate and effective. Boards should also consider whether oversight and management of climate-related risks and opportunities is integrated into the issuer’s strategic plan and should assess the effectiveness of the issuer’s climate-related disclosure controls and procedures to ensure the issuer’s principal risks are being identified and appropriately managed.

Build climate-related risks into business processes and management practices. Management is encouraged to consider which business divisions or units are responsible for identifying, disclosing and managing material climate-related risks; their reporting lines to senior management; and the extent to which these responsibilities are integrated into mainstream business processes and decision-making. Management should also consider whether it has implemented effective systems, procedures and controls to gather reliable and timely climate-related information for purposes of materiality assessments, management decision-making and disclosure to investors, regulators and other stakeholders.

Prepare voluntary climate disclosure with the same rigour as regulatory filings. If issuers provide voluntary climate-related disclosure in accordance with one or more available voluntary disclosure standards, there may be certain additional requirements and factors to consider. The 2019 Notice states that voluntary disclosure should be prepared with the same rigour as the issuer’s regulatory filings. Issuers should also consider the following when disclosing climate-related information on a voluntary basis:

- Material information in regulatory filings. Material information must be disclosed in regulatory filings. Boards and management should ensure that the materiality of information contained in any voluntary disclosure is assessed and, if the information is material, it must be disclosed in issuers’ AIF and/or MD&A. In addition, any voluntary disclosure should be consistent with the information included in continuous disclosure filings.

- No misrepresentations. Voluntary disclosure should not contain any misrepresentations and may be subject to civil liability for secondary market disclosure under securities laws. Boards and management should have a robust process in place for reviewing voluntary disclosure to ensure its reliability and accuracy.

- Obscuring of material information. Voluntary disclosure should not obscure material information.

Forward-looking information is subject to additional requirements. Issuers are reminded that if their disclosure contains forward-looking information (FLI), including information with respect to greenhouse gas (GHG) emissions targets or climate change scenario analyses, they must comply with the FLI requirements set out in NI 51-102. These include identifying the information as FLI, providing cautionary language, stating the material facts and assumptions used to develop the FLI, updating certain previously disclosed FLI and describing the issuer’s policy for updating FLI. The FLI requirements do not relieve issuers from disclosing material climate-related risks even if they are expected to occur or crystallize over a longer time frame.

Implications: Climate-related Disclosure Is Required

The 2019 Notice represents a clear signal to issuers that effective disclosure on climate-related issues is mandatory, not an option. Issuers have a responsibility to identify material climate-related risks and communicate information with respect to these risks and risk oversight in a clear, consistent and comprehensive manner. Issuers should consider both the 2019 Notice and the 2010 Notice when preparing their disclosure documents to ensure that both mandatory and voluntary disclosures comply with applicable securities laws and provide investors with meaningful information for making informed investment and voting decisions. These disclosures should be prepared under the proper oversight of the board and management, as appropriate.

Additional information about developments and trends in climate-related disclosure and sustainability reporting can be found in Davies Governance Insights 2018. Davies will continue to track and discuss developments regarding climate-related disclosure and reporting requirements and best practices, including in its Davies Governance Insights 2019 report expected to be released in the fall of 2019.

1 See section 4.5.1(ii)(C) – “TCFD Recommendations compared with current requirements in Canada” in SN 51-354.

2 See section 4.5.1(ii)(B) – “Climate change-related disclosure frameworks” in SN 51-354 and discussion at https://www.sasb.org/standards-overview/materiality-map/.